Tax Day

The tax season is finally open for individuals to submit their tax returns. This year the season is shorter compared all the other years. Submission of tax returns calls for proper planning to entail a smooth submission of returns.

Taxpayers need to ensure that they have allTaxpayersred documentation handy. These documents include IRP5, medical certificates, pension certificates, proof of medical expenses and all other relevant documents. If you are a first timer make sure you have registered with SARS and have a tax number. Once you get your tax number go on SARS efiling and create a profile. Once the profile has been created you can go ahead and submit your tax return.

Your accountant can help you with your individual tax returns by completing the return on your behalf and filing it through SARS efiling. Some taxpayers are not Tech savvy and prefer to submit their returns at the SARS branch close to them. This is time-consuming as one has to que at SARS to submit the tax return, I would advise that all taxpayers register of SARS efiling so they can submit their returns electronically from the comfort of their offices or homes. This is hustle free and very convenient.

An individual needs to ascertain if they have to submit a tax return. SARS has criteria to determine whether an individual taxpayer must submit a return information can be obtained on the SARS website.

For more information and assistance with your tax returns please do contact your accountant or tax practitioner who should be able to assist you with your tax queries or you can call SARS directly.

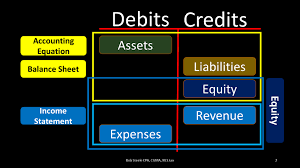

Business has its own language, just like any other career field. Knowing this language is crucial for every entrepreneur because information in business is communicated using certain essential financial accounting terms. As a business owner, it is important to familiarize yourself with these terms, especially as someone new to the business industry. They might seem intimidating at first, but when you get used to them, you will understand why you needed to know them.

Business has its own language, just like any other career field. Knowing this language is crucial for every entrepreneur because information in business is communicated using certain essential financial accounting terms. As a business owner, it is important to familiarize yourself with these terms, especially as someone new to the business industry. They might seem intimidating at first, but when you get used to them, you will understand why you needed to know them.